So far, there have been no explicit regulations and/or strategies/policies regarding the cultural and creative sectors (CCS) in Romania, though there are special laws governing certain segments of these sectors. These regulations are not systematically structured, which creates confusions, and conceptual and methodological difficulties.

The White Paper for Unlocking the Economic Potential of Cultural and Creative Sectors in Romania starts with a review of the performance of the cultural and creative sectors in recent years, highlighted by the evolution in turnover, number of employees, profit and labour productivity. The study also presents the issue of defining the cultural and creative sectors / industries. The European documents are still using both terms, i.e. “cultural and creative sectors” and “cultural and creative industries”, sometimes as synonyms, both referring to similar concepts such as the economy of culture, creative economy, knowledge-based economy/society etc. However, the European Commission document Green Paper – Unlocking the potential of cultural and creative sectors tries to harmonize the different approaches and to provide definitions that clarify the differences between the two concepts. According to this document, “cultural industries are those industries producing and distributing goods or services which at the time they are developed are considered to have a specific attribute, use or purpose which embodies or conveys cultural expressions, irrespective of the commercial value they may have”. Besides the traditional arts sectors (performing arts, visual arts, cultural heritage – including the public sector), they include film, DVD and video, television and radio, video games, new media, music, books and press. This concept is defined in relation to the cultural expression in the context of the 2005 UNESCO Convention on the protection and promotion of the diversity of cultural expressions.

The graphs below show the CCS’ dynamics over the period 2011-2015, with notice that the figures illustrate the evolution of the private sector only. It is worth mentioning that data regarding the evolution of the public sectors could not be isolated from the data on the overall public expenditures, simply because there are no itemized reports available as yet. This shortcoming can be addressed in the future, by a course of action designed to enable the clear determination of the exact share of public sector’s contribution to the development of the cultural and creative sectors.

The model suggested is of the ecosystem type and relies on the proximate type and on the specific difference between fields, taking into account not only the functions of culture and creativity, but also the way the cultural field is organised (public or private) and the type of stakeholders (independent artist, NGO, company or public institution). According to the given model in this document, there are three types of sectors: cultural, creative and transversal, with the following eleven sub-domains:

- Libraries and archives

- Cultural Heritage

- Crafts and handicrafts

- Performing Arts

- Architecture

- Book and Press

- Visual Arts

- Audiovisual and multimedia

- Advertising

- IT, software and electronic games

- Research – development

- The first three sub-domains are characterised by non-industrial cultural and artistic activities and are collectively referred to as culture and arts.

- The following three sub-domains have as a result the cultural expression and are regarded as cultural sectors.

- The following two sub-domains are functionality-oriented, but they have a cultural dimension and are deemed creative sectors.

- The last two sub-domains, known as transverse sectors, rely on creativity and innovation, are focused on functionality, but they are mainly used as support for the other sub-domains.

In some cases, the same domain or sector may be partly included in two groups, as it happens with crafts (included partly in the first group, as traditional crafts, partly in the intangible heritage category, and partly in the second group, as urban art crafts). Similarly, ICT is included partly in the third group, due to its computer games component, and partly in the fourth group, due to the rest of software activities.

Figure 1. Diagram of Cultural and creative sectors

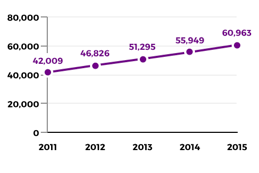

Graph. Evolution in the total number of CCS businesses over the period 2011-2015

Source: Borg Design Database, INCFC processed data

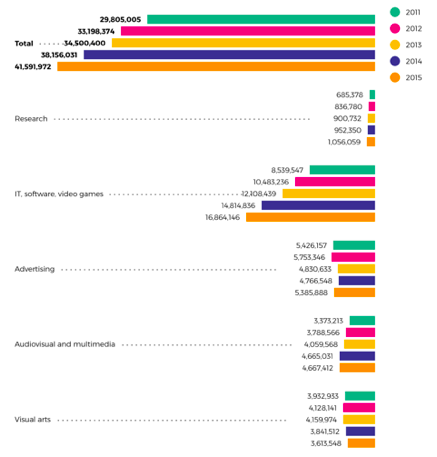

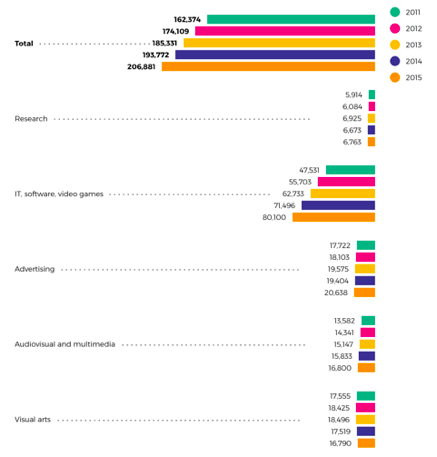

Total CCS turnover has increased in the period 2011-2015, from about 6 billion to almost 10 billion EUR. The biggest turnovers and the highest increase are recorded in the ICT sector (including software and electronic games), followed by books and press, advertising, audiovisual and multimedia and visual arts sectors. As for heritage, the performance analysis did not take into account the historical monument restoration works carried out through European funds or through national financing programmes, of which only a very small part can be partially found in the architecture chapter. Likewise, the analysis of the architecture sector took into account only the actual design activities and disregarded the construction or research-development related activities. At the same time, no specific surveys could be made regarding the turnovers generated by the heritage sector within cultural / sustainable tourism, education, research-development activities.

Graph. Evolution in turnover over the period 2011-2015 (part 1)

Source: Borg Design Database, INCFC data processing

Graph. Evolution in turnover over the period 2011-2015 (part 2)

Source: Borg Design Database, INCFC data processing

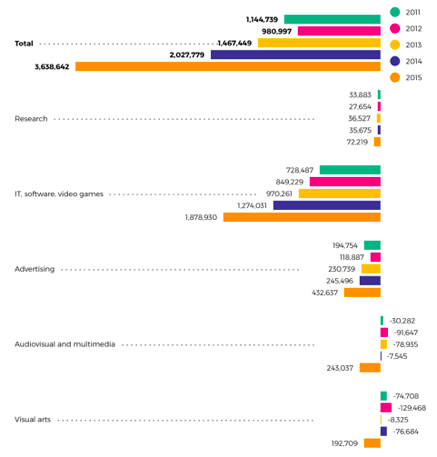

Profit has recorded the most spectacular growth, as it tripled during the analysed period from about 250 million EUR in 2011 to 800 million EUR in 2015. It is important to highlight that, again, the ICT sector stands on top in terms of growth rate, followed remotely by advertising and books and press sectors. It is worth pointing out the remarkable turnaround from loss to profit of the companies active in audio visual, media and visual arts (particularly design, photography and retail) sectors, in 2015.

Graph. Profit evolution in the period 2011-2015 (part 1)

Source: Borg Design Database, INCFC data processing

Graph. Profit evolution in the period 2011-2015 (part 2)

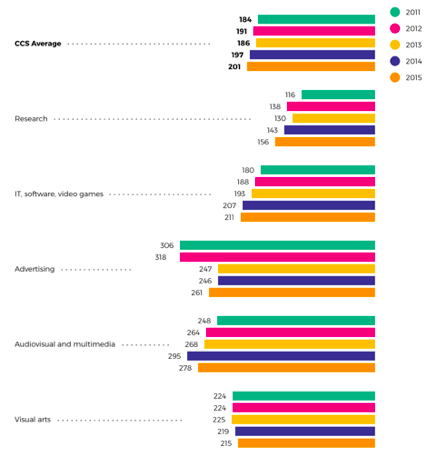

Regarding the evolution of the labour productivity, the national average rate has registered a slight increase in the analysed period, remaining close to the amount of 40,000 EUR (ratio between turnover and headcount). This time, the best performances are recorded in advertising and audiovisual and multimedia sectors, followed by visual arts and ICT, all these sectors exceeding the national CCS average in the period 2014-2015.

Graph. Evolution in labour productivity in the period 2011-2015 (part 1)

Source: Borg Design Database, INCFC data processing

Graph. Evolution in labour productivity in the period 2011-2015 (part 2)

Source: Borg Design Database, INCFC data processing

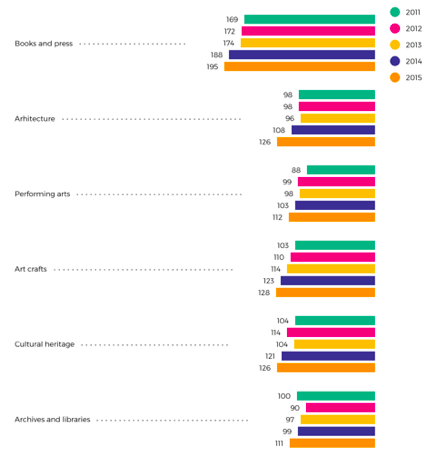

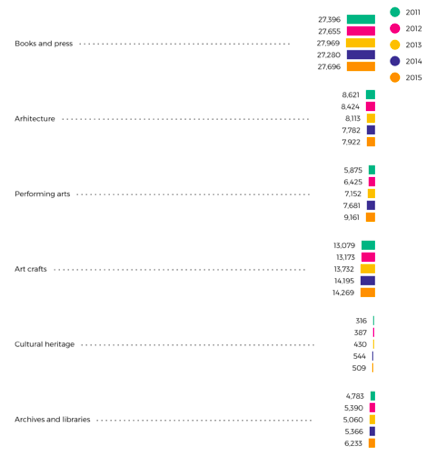

The number of employees in the cultural and creative sectors (mainly in the private sector) has recorded a slight increase in the period under review, remaining generally constant or, at times, with small fluctuations in certain sub-sectors.

Graph. Evolution of the number of employees by sub-sectors in the period 2011-2015 (part 1)

Source: Borg Design Database, INCFC data processing

Graph. Evolution of the number of employees by sub-sectors in the period 2011-2015 (part 2)

Source: Borg Design Database, INCFC data processing

The following objectives are recommended:

- Providing the necessary institutional support for the CCS by aligning agendas of various institutions and agencies on relevant government initiatives, including those relating to intellectual property protection, natural and cultural heritage, public procurement, taxation etc.

- Commitment of the government to implement policies and strategies dealing with the cultural and creative sectors and to promote the responsibilities of the local public authorities.

- Improvement and facilitation of the access to banking and non-banking finance of economic operators in the CCS.

- Catalyzing the spillover effects of the CCS into as many economic and social contexts as possible.

- Creation of an organisational culture to encourage participation in the public decision-making in favor of CCS entrepreneurship.

Comments are closed.